The biggest opportunity in banking right now is not a model, it is the gap that has formed.

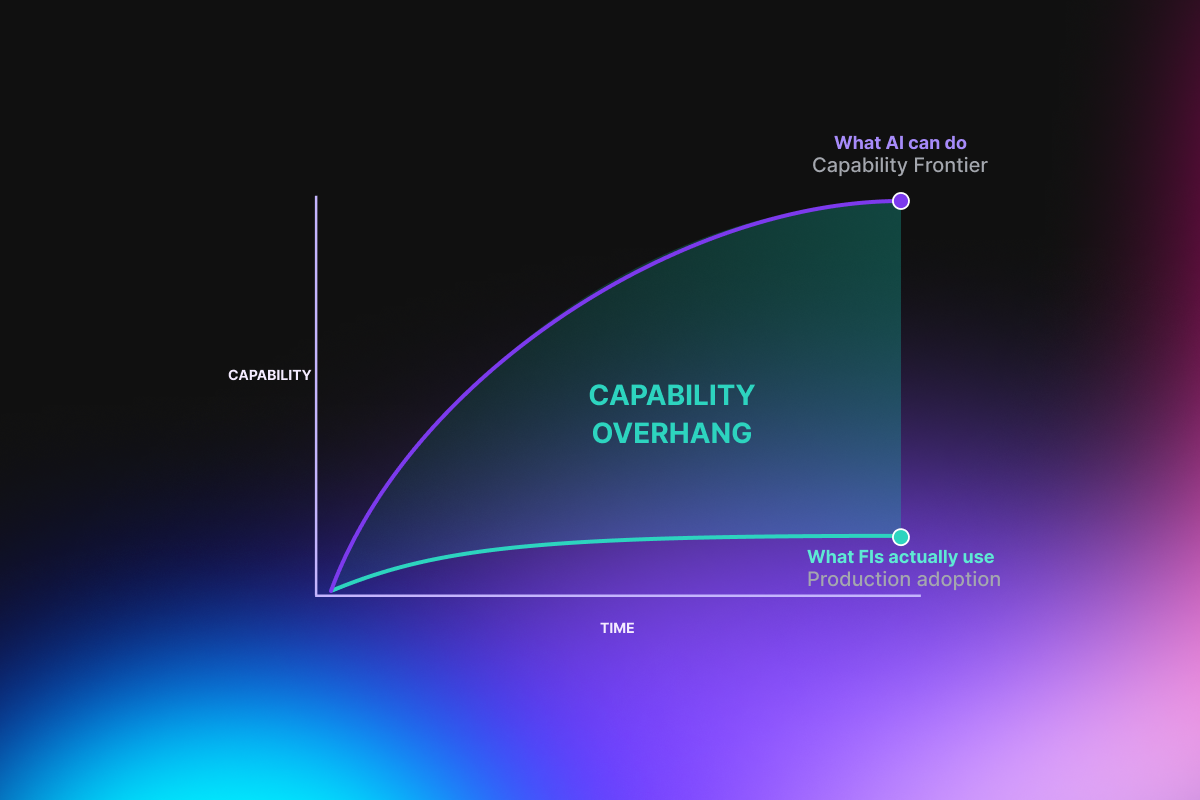

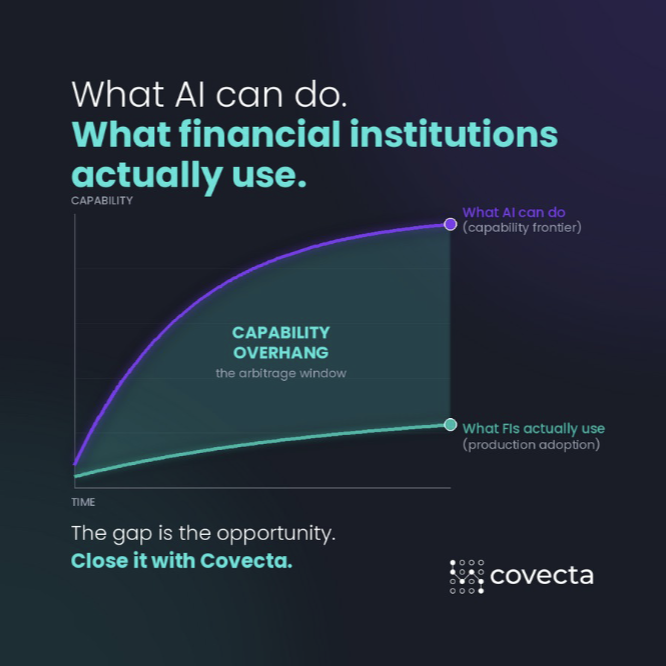

The gap between what AI can technically do today and what financial institutions are actually using it for is the widest it has been in any technology cycle I have lived through. This is the Capability Overhang. This is widening, rather than closing.

The arbitrage is real, and it is timed.

A capability overhang is not a permanent feature of a market. It is a temporary arbitrage window. The institutions that move now will capture compounding structural advantages: cost-to-originate falls, time- to-cash compresses, capacity expands, and the talent who want to do real work follow.

The institutions that wait will not catch up by buying a bigger model. The gap is not a model problem. It is a workflow problem. And workflows compound differently than software does. My read on the window: 18 months. Maybe less. Time is ticking.

What closing the gap actually looks like

Stop running pilots and pick a workflow with hard economics attached. Deploy vertical agents that already know how the work is done. Embed them where the work happens, with full traceability. Run

them to production, then scale to the next workflow. That is not a technology programme. It is an operating decision. And it is the only way the capability overhang gets closed inside a bank.

The window is closing Two years in the trenches has taught me that the institutions which win this cycle are not the ones with the biggest AI budget. They are the ones treating the workflow as the product, the agent as a colleague, and the next 18 months as the only window that matters. Let the team at Covecta help you capture the arbitrage.

So why is the gap widening?

Three reasons, all of which I have watched up close for the last two years building Covecta.

- AI is still being treated as a pilot, not a workflow. Banks run an isolated pilot in one team, measure a productivity uplift on one task, then declare success and stop. Pilots do not change cost-to-originate, it is workflows that do.

- The wrong tools are being deployed for mission-critical work. Horizontal models are landing in regulated workflows that need near-perfect precision, full traceability, and embedded domain knowledge. Consumer-grade AI tolerates 93 per cent accuracy, while Banking does not. Vertical AI, purpose-built for the work, is the only category that closes the gap in regulated environments.

- Agents still live in a separate window. Most "AI tools" in banks today live in a tab next to the work, not inside it. Agents have to be initiated where the work happens, integrated into the systems of record, capturing every step for audit and traceability. If your agent lives in a chat window, it is a copilot. If it lives in the workflow, it is a colleague.

What closing the gap actually looks like

Stop running pilots and pick a workflow with hard economics attached. Deploy vertical agents that already know how the work is done. Embed them where the work happens, with full traceability. Run them to production, then scale to the next workflow.

That is not a technology programme. It is an operating decision. And it is the only way the capability overhang gets closed inside a bank.

The window is closing

Two years in the trenches has taught me that the institutions which win this cycle are not the ones with the biggest AI budget. They are the ones treating the workflow as the product, the agent as a colleague, and the next 18 months as the only window that matters.