AI is going to change the way we live, the way we work, and the way we engage with society. In banking, that change already has a name most leadership teams have not yet said out loud: software has become a worker.

I want to make two arguments. The first is about how AI changes the nature of work in financial services. The second is a framework for judging how close your institution actually is to capturing it.

The evolution of software

Think about what software has been to us over time.

For a long time, software was a product. You bought it, you installed it, you owned a version until the next one came along. Then, over the last twenty years, it became a service. Software as a service is the model we all now take for granted: always on, continuously updated, rented rather than owned.

We are now entering a third era. Software as a worker. This is a fundamental shift in the way we think about technology and the relationship humans will have with it. And it changes four things at once.

Software now does the work. It does not just record it. The previous generation of enterprise software was a system of record: a place to log what a human had already done. Software as a worker completes the work itself. The output is the deliverable, not the database entry.

It sits within the org chart, not next to the worker. Software used to live on the desk beside the underwriter, the analyst, the credit officer. Now it sits inside the team, on the rota, in the job description. It is a colleague with a workload, not a tool waiting to be picked up.

The buyer changes. When software does the work, the decision moves from IT to the functional teams where the work is actually done. The people who own the outcome start owning the purchase.

Pricing moves from seats to outcomes. Per-seat licensing was a way to charge for access. When software produces work, you pay for the work it produces, not the number of people allowed to log in.

So the obvious question becomes: what skills should you expect from software as a worker?

A horizontal AI worker arrives on day one with no domain context. It can write a polite email. It cannot pass a credit committee. A vertical AI worker, built for a specific industry and a specific workflow, arrives knowing the credit memo, the covenant call, the KYC file. That is the difference between hiring a generalist temp and hiring a seasoned operator on day one. And in a regulated institution, that difference is everything.

This will change how our teams are organised and how they execute their work. Which brings me to the second argument.

The capability overhang

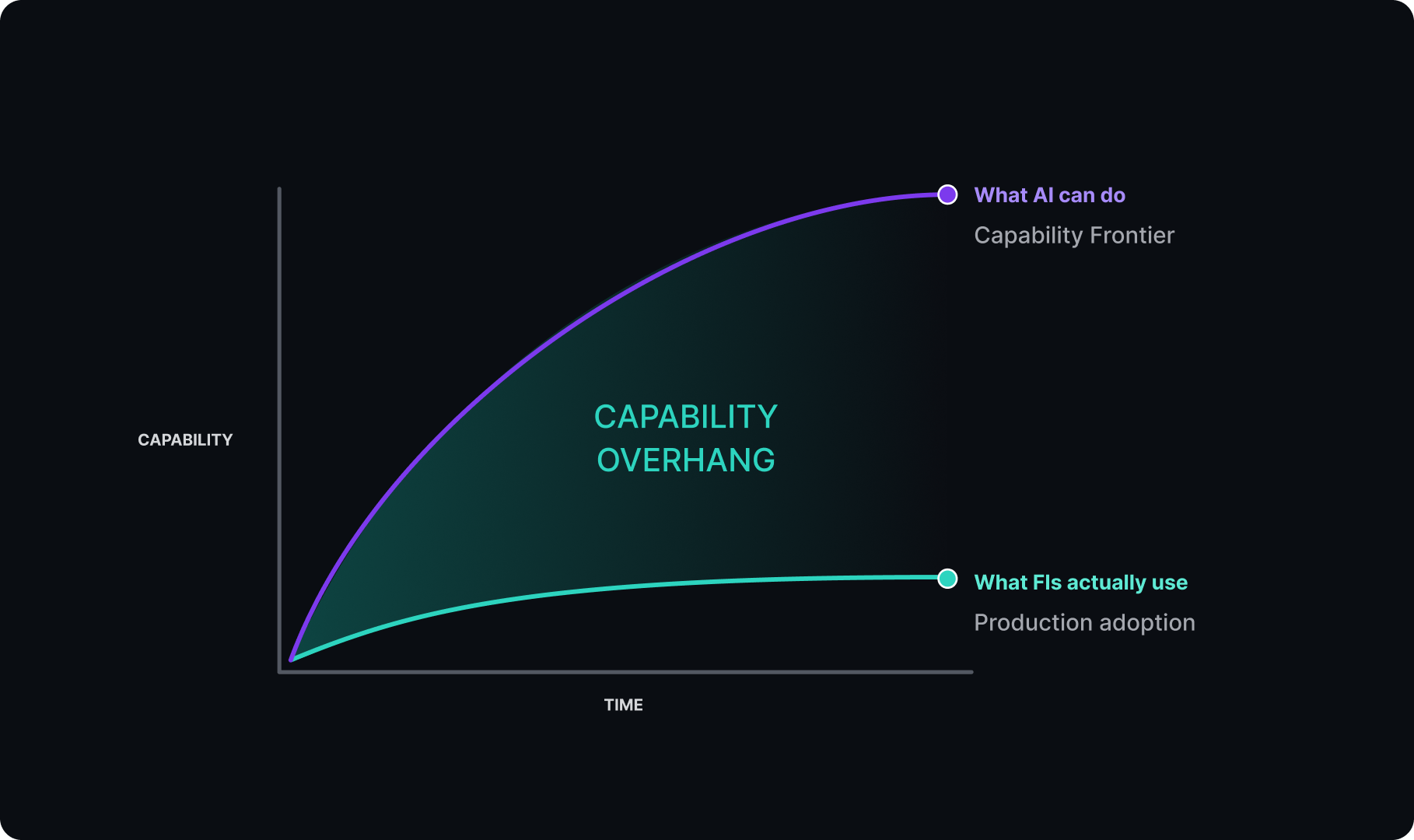

Over the last twelve months a capability overhang has formed. A capability overhang is the distance between what the technology can do and how much of it industry has actually adopted.

Like every technology cycle, this one has opened a temporary arbitrage window. History tells us these windows do not stay open for long, and this one is already closing. The institutions that close the gap first do not just get a head start. They get a structural advantage that compounds over time.

Here is what has changed. The constraint used to be technical. It no longer is. The constraint today is organisational and cultural. The next eighteen months will define the next decade of banking.

It is worth being precise about why the overhang exists, because the usual explanations are wrong.

It is not a lack of ambition. Every CEO has AI on the agenda. It is not a lack of budget: trillions are spent globally on technology and labour every year. And it is not, for the most part, a lack of talent. The gap exists for three specific reasons.

One: AI is still treated as a pilot, not put into production

Too many initiatives sit on an innovation roadmap, in a sandbox, owned by an innovation team, disconnected from the functions that run the institution. Nothing is fully optimised for a mission-critical workflow. Nothing crosses functional lines.

Being in production means something quite different. It means agents are integrated into your systems and work alongside your teams. It means you are rewiring workflows, not just running an isolated use case. The distance between a promising pilot and a production deployment is where most of the value is currently trapped.

Two: the wrong tools are selected for the wrong job

This is a major driver of the overhang. For the last two years, the loudest story in AI has been the horizontal copilot: generic, cross-industry, available off the shelf to all staff. These tools have done genuine work, and I do not want to dismiss that.

But here is what they cannot do. A horizontal copilot cannot read a credit memo and tell you whether the borrower's debt service coverage ratio is in line with policy and covenants. It cannot review your portfolio, recommend a policy change to compliance, and then update every active agent to reflect it. This is not a flaw in the technology. It is a feature of where horizontal copilots sit on the value chain.

Financial services is not a horizontal industry. It is built on policy, on judgement, on regulation. It carries roughly a hundred and fifty years of accumulated practice in how to lend, how to take deposits, how to protect customers, and how to evidence every decision to a regulator who may ask a question about it five years from now.

Vertical, domain-deep expertise is what delivers against that. It is aware of the regulatory frameworks, the audit trail and the policy. It understands that a credit memo is not just a document, but a relationship that lives across time and across systems. Vertical AI is the bridge between pilot and production in a regulated institution. It is the difference between an agent that can draft a marketing announcement and one that can run a fully deterministic covenant test that will get signed off.

Three: agents live in a separate window instead of inside the workflow

There is a real difference between an agent that completes a use case and one that is embedded in a workflow. Use-case agents tend to be deployed in a new browser tab or a sidebar. They leave too much manual effort with the user, who becomes the integration layer, copying context in and pasting output back out.

Agents that deliver inside the workflow are the ones that close the capability overhang. Four requirements have to be met to get there:

1. Agents are initiated from where the work begins.

2. Agents can pull data and context from the source systems.

3. An agent's output lands back inside the system of record.

4. The inputs, the decision and the output are fully auditable.

Meeting those requirements takes integration depth, a consistent user experience, and the ability to run inside complex, multi-step workflows. It means agents do not live in silos, sitting on top of your CRM or your loan origination system in isolation. The real promise is that AI works through your entire stack, alongside other agents, surfacing work and insights you have not seen before. It is the promise that AI optimises your institution, not just accelerates a single use case.

What we are building

That is the theory. Let me be transparent about the bias behind it, because I am building in this space.

We founded Covecta to be exactly what the horizontal copilots and the standalone models are not. We build Seasoned Banker Agents: domain experts in software form, specialists in the workflows that actually run a financial institution, across lending, accounts and deposits, and compliance.

We are live today. Not just with use cases, but with workflows, working with clients in production across the UK and the US, helping them drive adoption and accelerate out of the capability overhang.

Our core conviction is simple: the model is not the product. The value is in deploying a complete AI system, one that understands how your teams operate and how to motivate them, understands your customers and what makes them successful, and understands your technology and data and how to optimise it. We call that system our agent harness. The underlying model matters, but on its own it is an engine without a vehicle.

The window is closing

The capability overhang is real, and it is large. It is closing fast, and most boards and executive teams have not yet adjusted.

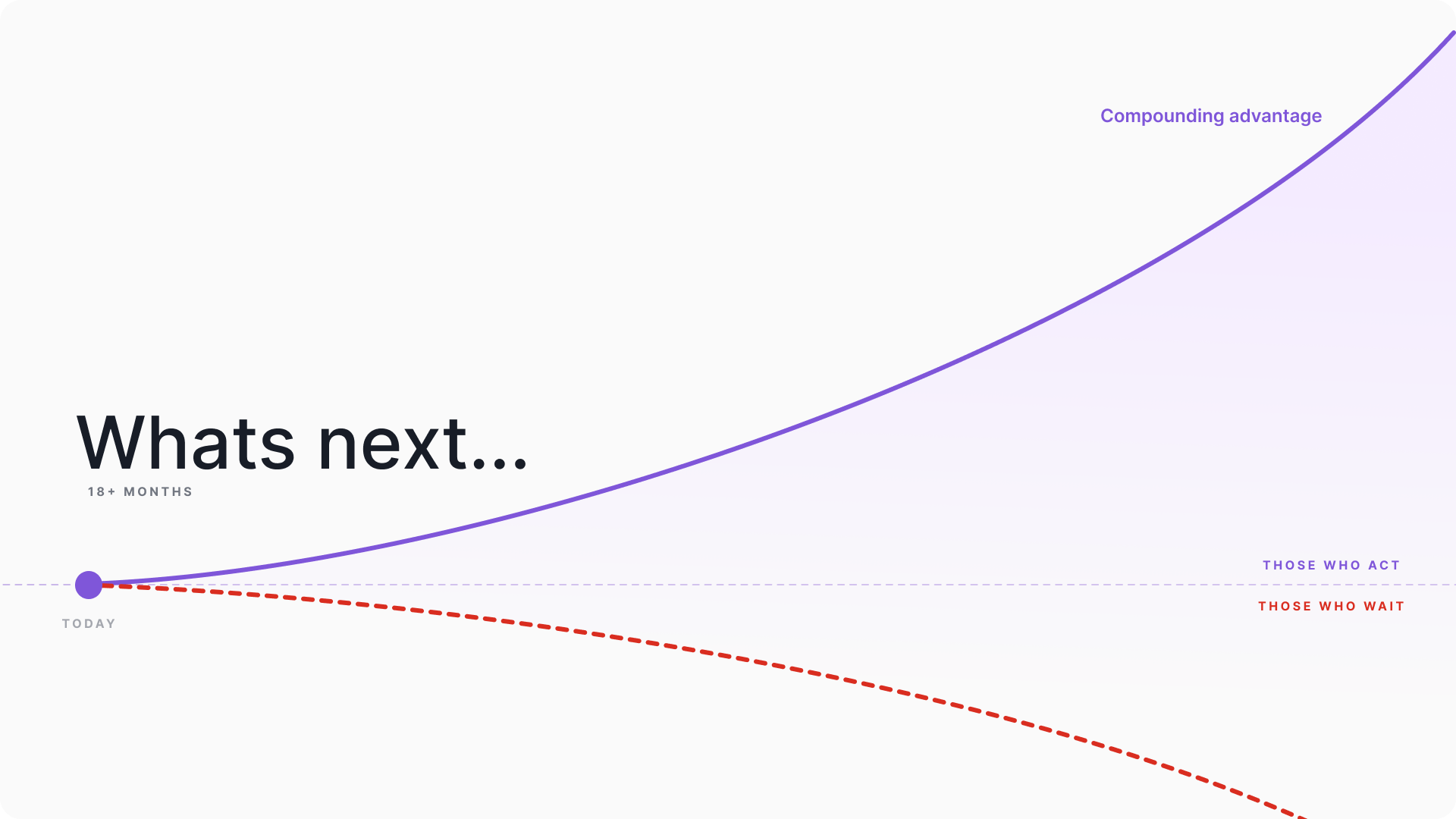

The next eighteen months will be a critical window, and the institutions reading this get to decide what they do with it. Some will spend it adding another pilot to an innovation pipeline. Some will spend it negotiating seat licences with a horizontal copilot vendor. And some, the ones we will be reading about in two years' time, will spend it rewiring how their institution actually operates.

To start, you do not need certainty. You do not need a perfect end-state architecture. You need a posture, and the courage to move from pilot to production. You need to choose vertical depth over the horizontal demo. You need to start if you have not, and accelerate if you have.

The window is closing. Those who can, must.

%201.png)