%201.png)

For thirty years, we've measured progress in banking software by counting systems and ever more capabilities on different screens. More dashboards. More tabs. More fields with little red asterisks demanding you fill them in before you're allowed to continue. We called this "digital transformation." A lot of it was data entry with a veneer.

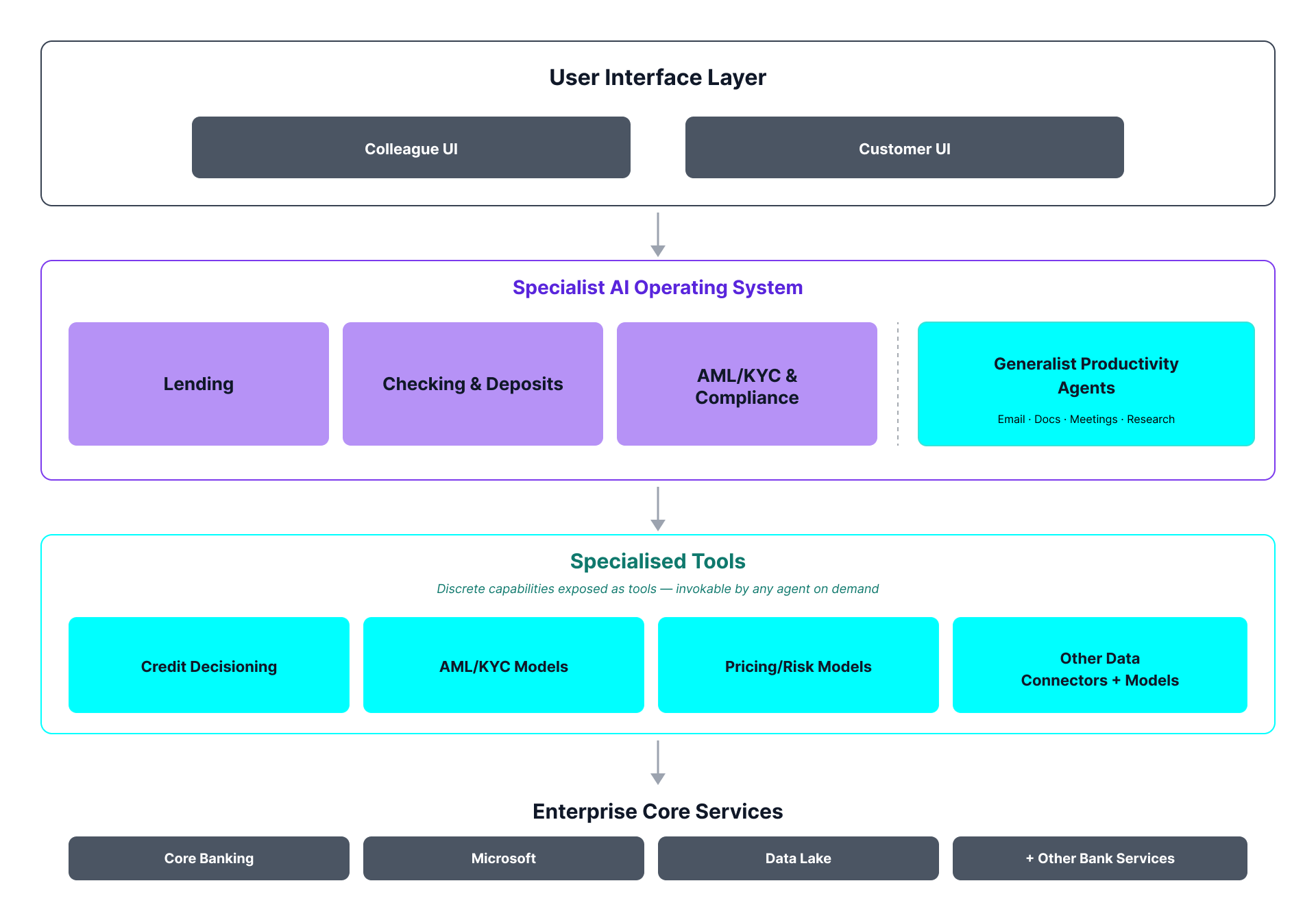

That time has come to a close. Fast. The next commercial bank won't be defined by a slicker app for humans to type into. It'll be defined by what sits underneath it: an AI operating system - not another tool in the stack, but an operating layer that runs across the whole stack and actually does the work.

Here are five predictions about how that will play out. I've tried to keep the buzzwords to a minimum, mostly because I find them as exhausting as you do.

Users will touch radically fewer interfaces - and those that persist shall wield radically more capability.

The best interface is the one you never had to learn. Today a relationship manager swivels between fourteen systems to onboard one client. Tomorrow they describe the outcome they want, and the work happens. The surface area shrinks to a conversation and a clean audit trail, while the capability behind it explodes. Screens were always scaffolding for humans doing the computer's work. When the computer does its own work, the scaffolding comes down.

Take lending, for example. In today's world of data availability there's no reason you shouldn't be able to say something to the effect of "British Airways is after a term loan for £50m" and then have absolutely everything that needs to come next, orchestrated for you, across all domains in the bank - engaging you only where genuine subjectivity and/or expert opinion is required. How often is this repeated across so many interfaces that do nothing but proudly show you what you've already done?

Whilst I'm not quite ready to state screens will have completely disappeared in banking in the short to medium term (nothing personal, Sam Altman & Jony Ive - I'm hopeful), I would assert this: if in two years' time your RMs are still having to navigate more than three interfaces to do their job - interfaces that likely look drastically worse than the internet banking experience you give customers - your AI transformation has failed, and most of your good RMs will have left.

Most systems become a tool an agent can call - or get found out.

Building on the above: software that was genuinely valuable will happily reinvent itself as something an agent can consume - an API, a tool, a capability. Commercial banks will need a huge number of these extremely valuable components (many of them becoming a bank's genuine IP - a rating model, say), discoverable by agents, to deliver the transformation we've long been promised. Software that was really just a glorified data-entry form - somewhere for a human to retype numbers from one place into another - has a rather large problem, because agents don't need somewhere to type. As banks increasingly look to big data strategies to master and allow for discoverable & aggregate data, the true utility of these discrete systems will be laid bare.

As Warren Buffett put it, "Only when the tide goes out do you discover who's been swimming naked." The AI operating system is the tide going out on enterprise software. A surprising number of "platforms" are about to be revealed as a login screen wrapped around a form. Every potential buyer should be pressing vendors to prove why they don't belong in that category.

Analytics stops being a monthly report and becomes the entire game.

Every bank is sitting on a goldmine without the correct tools. The ore is there - buried in PDFs, core systems, credit memos, email threads, and a spreadsheet someone named FINAL_v7_USE_THIS.xlsx. The real promise of AI was never the chat box. It's the ability to aggregate fragmented data, structure the unstructured, and then interrogate it on demand - building up proprietary datasets that no competitor has and no vendor can sell you.

This should have banks rushing to an AI operating system. Take lending again: think of all the rich data such a system would touch, from origination right through into monitoring. Tune that same intelligence to understand the aggregate of the portfolio, the bank's capital constraints and its performance, and there's no reason it can't already be making proactive suggestions on how to optimise in real time - flagging where to trim concentration, where appetite will be breached two quarters out, which exposures to reprice, and where capital is working hardest. That is a bank quietly optimising itself, in real time, on data only it holds and removes the quarterly cycles trying to connect strategy to execution, which if we're honest were too often guesswork.

The moat moves from doing the work to proving it was done right.

When an agent can do almost anything, the scarce resource becomes confidence that it did the right thing. Governance, explainability, and the well-placed human-in-the-loop stop being the compliance tax and start being the competitive edge. The banks that win will treat "show your working" as a feature, not a burden - because in a world of capable agents, trust is the product.

I've seen so many otherwise very clever people showcase an agent producing a single output they heavily prompted over a weekend - then look dumbfounded when you ask how they'll prove it works at scale, and stand up to a regulator, by getting the same outcome when you run the same inputs a thousand times over.

As much as policy and process - and the tools that support them - will become the bank's enshrined IP, the ability to lead with evaluations & deterministic outcomes at scale, proving outcomes that make sense in financial services, will increasingly be the vendor's IP. Again, every buyer should be evaluating this ability closely before they commit.

Headcount stops scaling with volume, and the org chart quietly inverts.

Software as a worker is a revolution that's already here. For decades the equation was simple: more business meant more processing meant more people in the middle office. That link snaps. Growth decouples from headcount. The people don't vanish - they migrate to the edges where judgement and relationships actually live, supervising the agents instead of feeding them. Fewer hands doing the work; more minds deciding what good looks like.

We've moved from software as a product, to software delivered as a service, to software that augments teams and can outright replace tedious work. It's time to reflect that new reality in our full-stack operating model - and to stop treating the AI that's coming as just another system.

None of this is ten years out. The components exist now; what's missing is the nerve to rebuild around them rather than bolting a chatbot onto the side of 1998.

The bank of the future probably won't impress you with its app. It might not have much of an app at all. It'll impress you with what you can't see: an operating system doing the work, an analytics engine that knows the book better than any human could, and a thin, honest layer of people pointing the whole thing in the right direction, offering you exactly what you want, exactly when you need it.